Filing for bankruptcy can feel like hitting a major roadblock, especially when you need to get back on the road with a reliable car. You might be wondering, “How soon after filing bankruptcy can I actually buy a car?” The answer isn’t as simple as you might think.

It depends on several important factors that can affect your chances of getting a loan and the interest rates you’ll face. If you want to know exactly what steps to take and how to improve your chances of driving away with a new or used car sooner than you expect, keep reading.

This guide will clear up the confusion and help you make smart choices for your financial future.

Bankruptcy Types And Their Impact

Bankruptcy affects your ability to buy a car in different ways. The type of bankruptcy you file changes the timeline and options for car financing. Understanding these effects helps in planning your next steps.

Each bankruptcy type carries unique rules and impacts your credit differently. This section explains how Chapter 7 and Chapter 13 bankruptcies affect your chances of buying a car.

Chapter 7 Effects

Chapter 7 bankruptcy clears most debts quickly. It stays on your credit report for up to 10 years. Lenders see you as a higher risk during this time.

You may still buy a car soon after filing, but interest rates will be high. Some lenders offer loans with low down payments. Saving money before applying helps improve your chances.

Waiting about two years after filing increases loan approval chances. Your credit score starts to rebuild after bankruptcy discharge. Showing steady income and stable finances is important.

Chapter 13 Effects

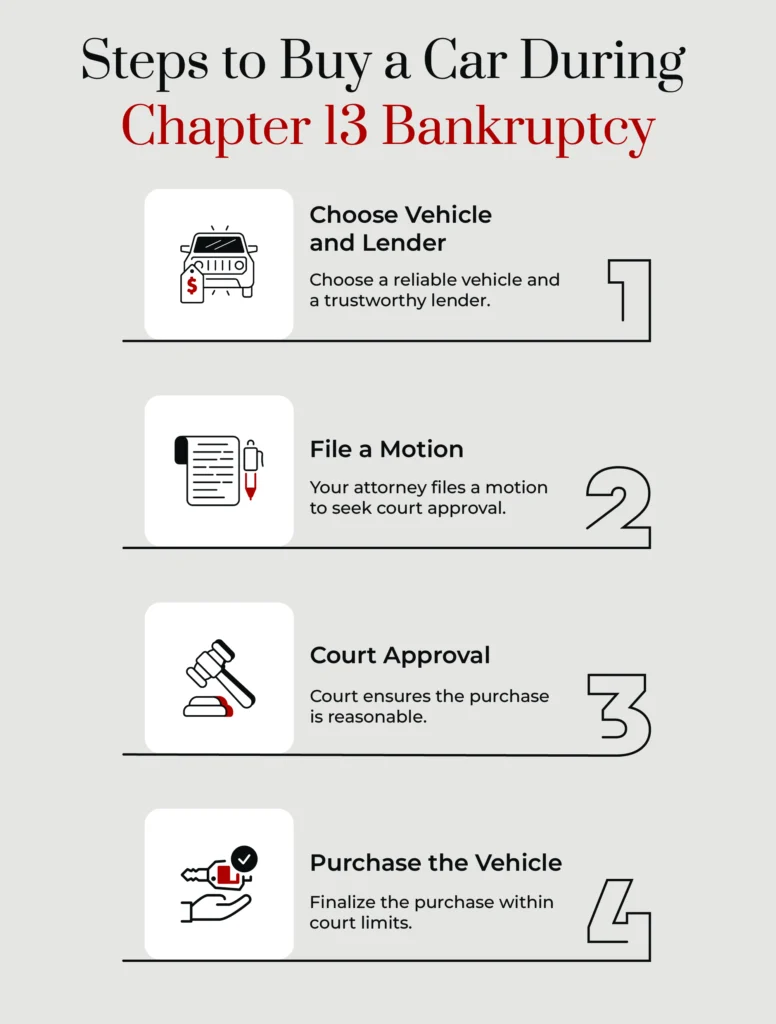

Chapter 13 involves a repayment plan lasting three to five years. You keep some assets and pay back part of your debts. This plan shows lenders your effort to fix credit.

Lenders may approve car loans during repayment with court permission. Payments might be smaller but interest rates stay higher than usual. Finishing the repayment plan improves credit faster.

Buying a car in Chapter 13 depends on income and court approval. Demonstrating a reliable budget and steady payments helps get better loan terms.

Credit: www.regalauto.com

Timing Your Car Purchase

Timing your car purchase after filing bankruptcy is important. It affects your chances of getting a loan and the interest rate you pay. Planning the right moment helps you save money and avoid stress. Understanding the waiting periods and other factors can guide your decision.

Waiting Periods To Consider

The time you must wait after bankruptcy varies by loan type. For a Chapter 7 bankruptcy, lenders often require two to four years. Chapter 13 bankruptcy usually has a shorter wait, about one to two years. Some lenders may offer special loans sooner, but with higher rates.

Waiting allows your credit score to improve. It also shows lenders you can manage money well after bankruptcy. Patience pays off with better loan terms and lower costs.

Factors That Influence Timing

Your credit score plays a big role in timing your purchase. The higher your score, the better your loan offers. Building credit after bankruptcy takes time and good habits.

Income stability matters too. Lenders want to see steady income before approving a car loan. Having a reliable job helps you get approved faster.

The type of car you want also affects timing. New cars usually need better credit than used cars. Choosing a used car may let you buy sooner after bankruptcy.

Financing Options Post-bankruptcy

After filing for bankruptcy, buying a car might seem tough. Financing options change, but they do exist. Knowing the types of loans helps you pick the best choice. This guide breaks down your options clearly.

Secured Vs Unsecured Loans

Secured loans require collateral, usually the car itself. This lowers risk for lenders. Borrowers often get better interest rates with secured loans. Payments tend to be lower and terms longer.

Unsecured loans need no collateral. They are riskier for lenders. Expect higher interest rates and stricter approval rules. These loans might be harder to get after bankruptcy.

Subprime Auto Loans

Subprime loans target buyers with low credit scores. Bankruptcy lowers credit scores, making subprime loans common. Interest rates on these loans are usually high. Loan terms might be shorter, with bigger monthly payments.

Subprime lenders focus on your ability to pay monthly. Proof of steady income helps approval chances. Saving for a bigger down payment also improves your options.

Credit: www.stoneroselaw.com

Improving Your Credit After Bankruptcy

After filing for bankruptcy, improving your credit is very important. A better credit score helps you buy a car sooner. It also opens doors to good loan offers and lower interest rates. The process takes time but starts with small steps. Focus on building habits that show lenders you manage money well.

Simple actions can make a big difference. Paying bills on time and using credit carefully helps rebuild trust. Each positive move adds to your credit history and score. Patience and discipline lead to steady progress.

Rebuilding Credit Scores

Start by checking your credit report for errors. Fixing mistakes can improve your score quickly. Next, apply for a secured credit card or a credit-builder loan. These tools help show you can handle credit responsibly. Keep balances low and pay off bills each month. Over time, this builds a positive credit record.

Make all payments on time. Late payments hurt your score. Avoid closing old accounts, as they add to your credit history length. Monitor your credit score regularly to track progress and adjust habits.

Using Credit Wisely

Use credit cards only for small, regular purchases. Pay the full amount every month to avoid interest charges. Keep your credit utilization below 30 percent. High balances can lower your score. Avoid applying for many new credit accounts at once.

Focus on steady, responsible credit use. This shows lenders you can manage debt well. Over time, your credit improves, and buying a car becomes easier and cheaper.

Tips For Buying A Car Soon After Bankruptcy

Buying a car soon after bankruptcy can feel hard. Many worry about loan approval and high costs. Smart tips help find good cars and better loan terms. These tips make the process clear and easier to handle.

Finding Affordable Vehicles

Choose cars that fit your budget. Used cars often cost less and still run well. Check online listings and local dealerships for deals. Look for cars with low miles and good reviews. Avoid new models that have high prices.

Consider vehicles with low insurance costs. Maintenance and fuel efficiency also save money over time. Take time to test drive and inspect before buying. Affordable cars mean less financial pressure after bankruptcy.

Negotiating Loan Terms

Prepare to discuss loan details with lenders. Compare interest rates from banks and credit unions. A lower rate saves money each month. Ask about the loan length and monthly payment options.

Show proof of steady income to build lender trust. A larger down payment may lower interest rates. Understand all fees before signing any loan papers. Clear terms avoid surprises and help manage payments.

Credit: www.youtube.com

Common Challenges To Expect

Buying a car soon after filing bankruptcy can be tough. Lenders see you as a higher risk. This means you may face several challenges. Knowing these challenges helps you prepare better. It also improves your chances of getting a loan.

Higher Interest Rates

After bankruptcy, expect higher interest rates on car loans. Lenders charge more to cover their risk. This means your monthly payments will be higher. Even if you qualify for a loan, the cost will be greater. It can add up to thousands more over the loan term.

Higher rates make it harder to afford a new car. Budget carefully and shop around for the best rate. Some lenders specialize in loans for people with bankruptcy.

Loan Approval Difficulties

Getting approved for a car loan is not easy after bankruptcy. Many lenders will deny your application. They see bankruptcy as a sign of financial trouble. This lowers your chances of approval.

Approval depends on your credit score, income, and job stability. Some lenders require a co-signer to reduce their risk. You may need to provide a larger down payment too. Patience and persistence are key during this process.

Frequently Asked Questions

How Soon Can I Buy A Car After Bankruptcy?

You can buy a car immediately after bankruptcy, but loan approval depends on your credit. Some lenders offer financing during bankruptcy with higher interest rates. Waiting 6 to 12 months after discharge improves your chances of better loan terms and lower rates.

Will Bankruptcy Affect My Car Loan Interest Rates?

Yes, bankruptcy typically results in higher interest rates on car loans. Lenders see you as a higher risk. Rates may be significantly above average for at least 1 to 2 years post-bankruptcy. Improving your credit score can help reduce rates over time.

Can I Get A Car Loan During Bankruptcy?

Getting a car loan during bankruptcy is possible but difficult. Most lenders require court permission or proof of income. Interest rates are often very high. Secured loans, where the car is collateral, are more likely to be approved.

Does Chapter 7 Or 13 Affect Car Buying Differently?

Yes, Chapter 7 discharges debts faster, allowing quicker car purchases. Chapter 13 requires court approval and a repayment plan, delaying buying. Chapter 13 may limit your budget due to monthly payments but can help rebuild credit steadily.

Conclusion

Buying a car after bankruptcy takes time and patience. Most lenders want to see you rebuild your credit first. This can take from a few months to a couple of years. Saving money for a down payment helps a lot.

Shop around for loans with fair interest rates. Keep your financial habits strong and steady. Soon, you will have a car and a better credit score. Remember, smart choices now lead to better opportunities later. Stay focused and keep moving forward.