Have you ever wondered if your car has gap insurance? It’s a question many drivers overlook until it’s too late.

Gap insurance can save you thousands of dollars if your car is totaled or stolen, but how do you know if you’re actually covered? You’ll discover simple ways to check your policy and understand what gap insurance really means for you.

Keep reading to protect yourself from unexpected expenses and drive with confidence.

Credit: www.skylacu.com

What Is Gap Insurance

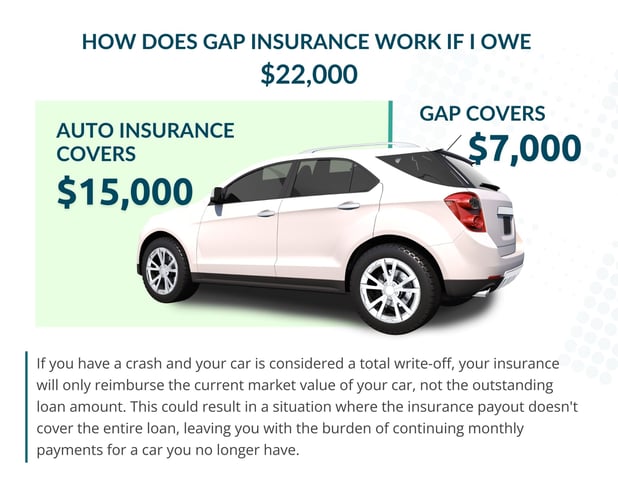

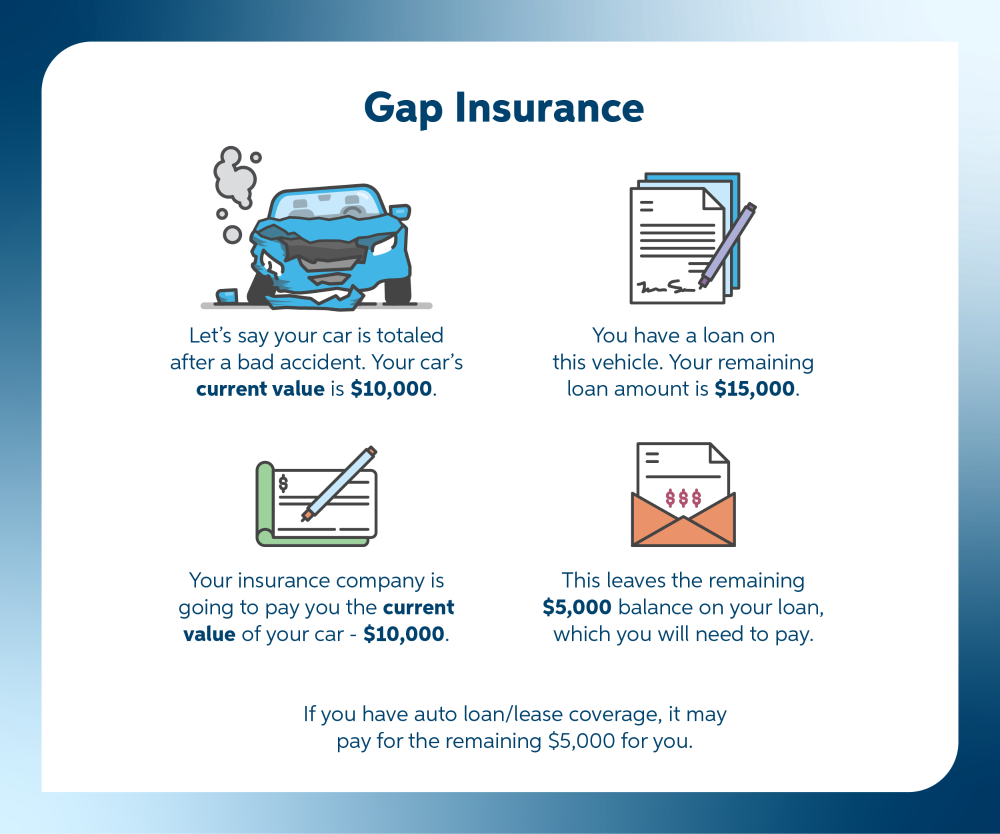

Gap insurance protects car owners from losing money after a car accident. It covers the difference between what you owe on your car loan and the car’s actual value. This insurance is useful when your car is totaled or stolen.

Cars lose value quickly. Sometimes, the loan balance is higher than the car’s market value. Gap insurance pays this “gap” so you don’t pay out of pocket.

What Does Gap Insurance Cover?

Gap insurance covers the difference between the car’s value and the loan balance. It pays if your car is totaled or stolen and not recovered. It does not cover repairs or your regular insurance deductibles.

Who Needs Gap Insurance?

Gap insurance is helpful for drivers who finance or lease new cars. It protects those who owe more than their car is worth. It is less useful for those who pay cash or have small loans.

How Is Gap Insurance Different?

Gap insurance is not the same as regular car insurance. Regular insurance covers damages and liability. Gap insurance only covers the loan balance difference after a total loss.

Why Gap Insurance Matters

Gap insurance helps cover the difference between your car’s value and what you owe. Check your insurance policy or ask your provider to see if you have it. This protects you from paying more after a total loss.

Gap insurance helps protect you from paying more than your car’s value. Cars lose value fast after purchase. This can leave a gap between what you owe and what insurance pays.

In case of theft or total loss, standard insurance pays the car’s current value. This value might be less than your loan or lease balance. Gap insurance covers this difference, saving you money.

Protecting Your Finances

Without gap insurance, you pay the difference out of pocket. This can be a large, unexpected cost. Gap insurance stops this financial burden. It keeps you from owing money on a car you no longer have.

Covering Loan And Lease Gaps

Loans and leases often have different payoffs than the car’s market value. This creates a “gap.” Gap insurance covers this gap. It ensures you don’t lose money if your car is totaled early.

Peace Of Mind On The Road

Gap insurance adds security. You can drive without worry. Knowing you won’t owe extra after an accident reduces stress. It helps you focus on safe driving instead of financial risk.

Where To Check Your Policy

Knowing where to check your gap insurance policy saves time and confusion. Gap insurance covers the difference between your car’s value and what you owe. It is important to confirm if you have this coverage before an accident or loss.

Check a few places to find out if your policy includes gap insurance. Your insurance documents, provider, and loan or lease agreement hold key information. Each source can tell you if gap insurance is part of your coverage.

Review Your Insurance Documents

Start by reading your insurance policy paperwork. Look for terms like “gap insurance” or “loan/lease payoff coverage.” Your declarations page might list it clearly.

Find the section that explains coverage types. It will describe if gap insurance is included and how it works. Keep these papers handy for future reference.

Contact Your Insurance Provider

Call your insurance company’s customer service. Ask directly if your policy has gap insurance. They can quickly check your account details.

Insurance agents explain your coverage in simple terms. They also tell you how to add gap insurance if you don’t have it. Keep the call notes for proof.

Check Your Auto Loan Or Lease Agreement

Review your loan or lease contract documents. Some lenders add gap insurance as part of your agreement. The contract will state if gap coverage is included or optional.

Look for sections about insurance requirements or protection plans. Confirm if gap insurance is bundled with your financing. This protects you from owing more than your car’s value.

Credit: www.auto-owners.com

Signs You Might Have Gap Insurance

Knowing if your car has gap insurance can save you money after a total loss. This type of coverage pays the difference between your car’s value and the amount you owe. Some signs can help you find out if you have this insurance.

Additional Premium Charges

Check your insurance bill for extra charges. Gap insurance often comes as a separate cost. This charge might appear as a small fee on your monthly or yearly premium. If you see a line item with “gap” or “loan/lease protection,” you likely have gap insurance.

Policy Coverage Details

Review your insurance policy documents carefully. Gap coverage is usually listed under special coverage or add-ons. The policy will explain what the coverage includes and the limits. Look for words like “gap coverage,” “loan balance,” or “difference coverage.” These terms show you have gap insurance.

Statements From Your Insurer

Contact your insurance company and ask directly. They can confirm if gap insurance is part of your plan. Some insurers send statements or reminders about gap coverage. These messages often come after you buy the policy or renew it. Keep an eye on any official letters or emails from your insurer.

How To Add Gap Insurance

Adding gap insurance protects you from paying the difference if your car is totaled. It covers the gap between what you owe and what your car is worth. There are three main ways to add this coverage. Choose the option that fits your needs and budget.

Through Your Insurance Company

Contact your current car insurance provider. Ask if they offer gap insurance as an add-on. Many companies offer it for a small extra fee. Adding it to your existing policy is simple and fast. Your insurer can explain the terms and costs clearly.

Via Your Car Dealer

Dealers often offer gap insurance at the time of purchase. They include it in your financing paperwork. This option may be convenient but sometimes costs more. Always ask for a clear price and details before agreeing. Compare with other offers to get the best deal.

Third-party Providers

Independent companies sell gap insurance separately from insurers or dealers. These providers often offer competitive rates. You can shop online or by phone. Check reviews and reputation before buying. Third-party gap insurance can be a flexible choice.

Common Misconceptions

Many people have wrong ideas about gap insurance. These mistakes cause confusion. Knowing the truth helps you decide better. Let’s clear up some common myths about gap insurance.

Gap Insurance Is Mandatory

Gap insurance is not required by law. Some think it is, but it depends on where you live. Car dealers might suggest it, but you can choose to buy or skip it. Always check your own needs before deciding.

It Covers Everything

Gap insurance does not cover all damages. It only pays the difference between your car’s value and what you owe. Repairs, injuries, or theft may need other insurance. Know what your policy includes.

It’s Only For New Cars

Gap insurance is not just for new cars. It can help with used cars too. If you owe more than the car’s value, gap insurance can protect you. Age or type of car does not limit coverage.

Cost Factors For Gap Insurance

Gap insurance costs vary based on several important factors. Knowing these can help you estimate how much you might pay. Understanding cost drivers also aids in making smart decisions about coverage. Below are key elements that affect gap insurance pricing.

Vehicle Depreciation

Cars lose value fast after purchase. Gap insurance cost depends on how quickly your car’s value drops. Newer cars or luxury models often have higher depreciation rates. Faster depreciation means a higher chance you owe more than the car’s worth. This raises the price of gap insurance.

Loan Or Lease Balance

The amount you owe on your loan or lease matters. Gap insurance covers the difference between the car’s value and what you still owe. Larger loan balances increase the coverage needed. More coverage usually means higher insurance costs. Shorter loan terms can lower the cost because you owe less over time.

Insurance Provider Rates

Each insurance company sets its own prices. Rates depend on the provider’s policies and risk assessment. Some providers charge more for gap insurance than others. Shopping around can help find a better rate. Your credit score and location can also affect the price.

When To Use Gap Insurance

Gap insurance covers the difference between what you owe on your car and its actual value. It helps in situations where your car is totaled or stolen. Knowing when to use gap insurance can save you money and stress.

When Your Car Is Totaled

Car insurance pays the current market value after a total loss. Sometimes, this amount is less than your loan balance. Gap insurance covers this gap to avoid paying out of pocket.

When Your Car Is Stolen

If your car is stolen and not recovered, your insurance pays only its value. Gap insurance covers the remaining loan amount you owe to the lender.

When You Owe More Than Your Car’s Worth

New cars lose value quickly, especially in the first year. This can leave you owing more than the car is worth. Gap insurance protects you during this time.

When You Made A Small Down Payment

Small down payments increase the chance of owing more than the car’s value. Gap insurance helps cover the difference if your car is lost or damaged.

Credit: www.hondauniverse.com

Frequently Asked Questions

How Can I Check If My Car Has Gap Insurance?

Contact your auto insurance provider directly. Ask if your policy includes gap coverage. Review your insurance documents for gap insurance details.

Does My Car Loan Include Gap Insurance Automatically?

Not always. Some lenders offer gap insurance with loans. Check your loan agreement or ask your lender to confirm.

Can My Car Dealer Provide Gap Insurance Information?

Yes, dealers often offer gap insurance. Ask your dealer if gap coverage was included in your purchase or financing package.

Where Else Can I Find Proof Of Gap Insurance?

Check your insurance declarations page or policy documents. Your insurer’s online portal may also show gap insurance details.

Conclusion

Knowing if your car has gap insurance helps protect your finances. Check your insurance policy or ask your agent directly. Gap insurance covers the difference if your car is totaled. It is important for new or leased vehicles. Keep your documents in a safe place for easy access.

Understanding your coverage brings peace of mind on the road. Stay informed and review your insurance regularly. Protect yourself from unexpected expenses with the right knowledge.