Are you wondering how long you can get a car loan for? Knowing the right loan length can save you money and stress.

Choosing the right loan term affects your monthly payments, interest rates, and overall cost. You’ll discover the typical loan periods, how they impact your budget, and tips to pick the best option for your needs. Keep reading to make a smart decision that fits your financial goals perfectly.

Credit: cainandherren.com

Car Loan Durations

Car loan durations vary widely depending on the lender and borrower needs. Choosing the right loan length affects monthly payments and total interest paid. Shorter loans cost more per month but less overall. Longer loans lower monthly costs but increase total interest. Understanding loan terms helps make better financial decisions.

Common Loan Terms

Car loans often last between 24 and 72 months. The most common terms are 36, 48, 60, and 72 months. Some lenders may offer loans as short as 12 months or as long as 84 months. Shorter loans have higher monthly payments but save money on interest. Longer loans make payments smaller but increase total interest cost. Choose a term that fits your budget and goals.

Short-term Vs Long-term Loans

Short-term loans usually last 12 to 36 months. These loans require higher monthly payments. Paying off the loan faster means less interest overall. Long-term loans run from 48 to 84 months. They lower monthly payments, easing monthly budgets. But they cost more in total interest. Think about how much you can pay monthly. Balance monthly cost with total loan cost.

Factors Influencing Loan Length

Several factors affect how long you can get a car loan. Lenders consider different aspects before deciding loan length. Understanding these factors helps you choose the right loan term. Shorter loans cost less interest but have higher monthly payments. Longer loans lower monthly costs but increase total interest paid.

Credit Score Impact

Your credit score plays a big role in loan length. Higher scores often get shorter loan terms with better rates. Lower scores may lead to longer loans to reduce monthly payments. Lenders see good credit as less risk, so they offer better terms. Poor credit means lenders want more time to get paid back.

Loan Amount And Interest Rates

The amount you borrow influences the loan term. Larger loans might have longer terms to keep payments affordable. Interest rates also affect how long loans last. Higher rates increase monthly payments, so lenders may extend the loan length. Lower rates allow for shorter loans with manageable payments.

Vehicle Age And Type

New cars usually qualify for longer loan periods. Older cars might get shorter loans due to faster depreciation. Lenders see used cars as riskier, so they limit loan length. The type of vehicle matters too. Luxury or specialty cars might have different loan options. Overall, newer and common cars get better loan terms.

Benefits Of Different Loan Terms

Choosing the right car loan term affects your budget and overall cost. Different loan lengths offer unique benefits. Knowing these helps you pick the best option for your needs.

Shorter loan terms usually mean higher monthly payments. But they save money on interest and clear your debt faster. Longer loans lower monthly costs but increase total interest paid over time.

Advantages Of Shorter Loans

Short loans reduce the total interest paid on your car. You own the car outright sooner. Higher monthly payments build equity faster. This option suits those with steady income. It helps avoid long-term debt. You pay less in the long run.

Advantages Of Longer Loans

Long loans offer lower monthly payments. This eases monthly budget stress. More people can afford newer or better cars. Payments stretch over several years, making them manageable. This term fits tight budgets or irregular income. You get flexibility but pay more interest overall.

Risks Of Extended Loan Periods

Choosing a longer car loan period might seem helpful. It lowers monthly payments but carries risks. Extended loans can cost more and create financial problems. Understanding these risks helps make smart decisions.

Higher Interest Costs

Longer loan terms mean paying interest for more years. Interest adds up and increases the total cost of the car. Even if monthly payments are lower, the overall price is higher. This can make the car much more expensive than its actual value.

Negative Equity Concerns

Cars lose value quickly after purchase. With long loans, the car may be worth less than what you owe. This situation is called negative equity. It makes it hard to sell or trade the car. You might still owe money even after selling the vehicle.

Choosing The Right Loan Term

Choosing the right loan term is key when buying a car. The loan length affects your monthly payments and total cost. Picking a term that fits your money and plans helps you stay comfortable and avoid stress. This section explains how to match your loan term with your budget and goals.

Budget Considerations

Shorter loan terms mean higher monthly payments but less interest overall. Longer terms lower monthly costs but increase total interest paid. Think about your income and bills. Can you pay more each month without trouble? A clear budget helps you pick a term that fits your money. Avoid stretching your budget too thin. This keeps your finances stable.

Financial Goals Alignment

Your loan term should match your financial goals. Want to pay off your car fast? Choose a shorter term. Want lower monthly payments to save cash? Pick a longer term. Also, think about other goals like saving for a home or retirement. The right loan term supports your bigger money plans. Balance paying for your car and reaching other goals.

Credit: www.labiosthetique.ee

Tips To Get Better Loan Terms

Getting better loan terms can save you money and stress. Small changes can lead to lower interest rates and longer repayment periods. Follow these tips to make your car loan more affordable and flexible.

Improving Credit Score

A higher credit score gets better loan offers. Pay bills on time every month. Reduce credit card debt to lower your credit usage. Check your credit report for errors and fix them quickly. A good credit score shows lenders you are responsible.

Negotiating With Lenders

Talk directly with lenders about your loan options. Ask for lower interest rates or longer repayment terms. Show them your good credit score and steady income. Don’t accept the first offer. Negotiation can lead to better deals and savings.

Exploring Different Lenders

Compare loan offers from banks, credit unions, and online lenders. Each lender has different rates and terms. Credit unions often offer lower rates than banks. Online lenders may provide faster approval. Checking many options helps you find the best loan.

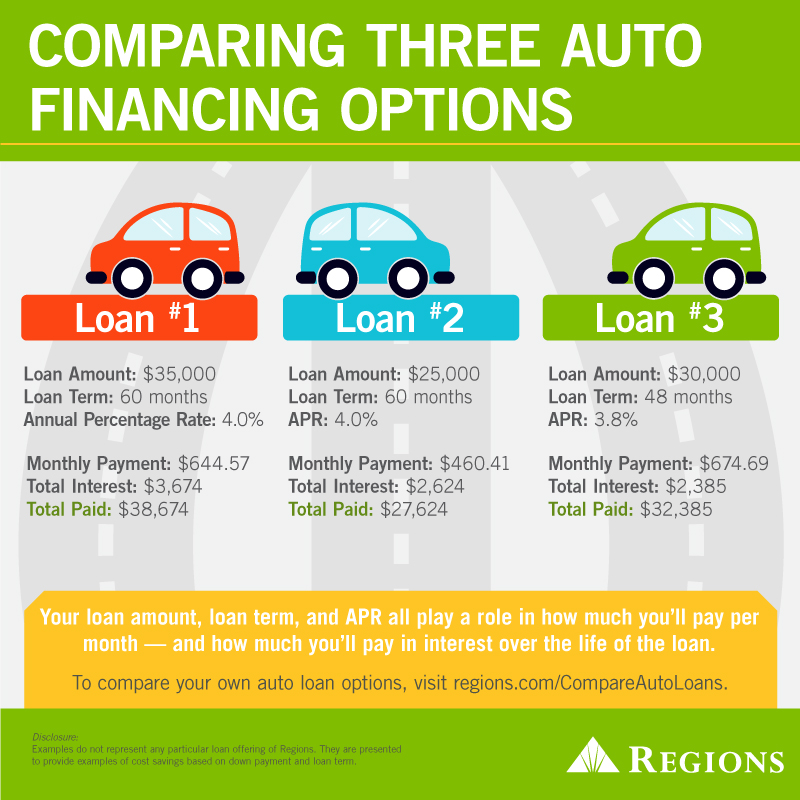

Credit: www.regions.com

Frequently Asked Questions

What Is The Typical Maximum Term For A Car Loan?

Most car loans last between 36 to 72 months. Some lenders offer up to 84 months, but longer terms can increase interest costs.

How Does Loan Length Affect Car Loan Payments?

Longer loan terms lower monthly payments but increase total interest paid. Shorter terms cost more monthly but save money overall.

Can Loan Duration Impact Car Depreciation Risk?

Yes, longer loans may exceed the car’s value due to depreciation. This can leave you owing more than the car is worth.

Are Longer Car Loans Better For Credit Scores?

Longer loans can improve credit by showing consistent payments. However, missed payments on long loans can harm your credit more.

Conclusion

Car loans can last from a few months up to seven years. Longer loans mean smaller monthly payments but more interest overall. Shorter loans cost less in interest but need higher payments. Choose a term that fits your budget and goals.

Understand the total cost before signing. Clear loan terms help avoid surprises later. Think about how long you want to keep the car. Balance monthly cost and total price carefully. This helps you make a smart loan decision.